Companies like CVS and UnitedHealth are now some of the world’s biggest businesses. Is that healthy for the rest of us?

In April, the corporate behemoth that started life as the Consumer Value Store celebrated its 60th birthday with a costume party. Karen Lynch, the CEO of what is now CVS Health, asked her top executives to attend a town hall dressed in 1960s fashion. Some opted for tie-dye, some opted out. Lynch herself enthusiastically embraced the brief, donning the white go-go boots and pillbox hat of a Mad Men–era flight attendant.

But while Lynch was cosplaying as a woman with little professional power, she was celebrating the latest acquisition in her career as a health care mogul. She joined CVS in 2018 when the pharmacy chain paid $70 billion to buy Aetna, the insurance giant that now covers about 37 million Americans. Since becoming CEO of the combined company in 2021, Lynch has spent another $19 billion on primary care and home health care businesses, betting that CVS can profit by directly owning doctors’ groups.

By her side at that birthday party was Mike Pykosz, CEO of primary care company Oak Street Health. The Chicago-based business specializes in treating Medicare-eligible—and thus highly profitable—patients; Lynch was in the process of bringing Oak Street and its 600 physicians and other providers under CVS’s ever-expanding umbrella. A few weeks later, CVS closed the deal. And Lynch saw the number of people whose health and lives are affected by her decisions expand again, to more than 110 million.

“I always think, sitting in this chair, ‘How would I want to be treated? How would I want my family members to be treated?’ ” Lynch tells Fortune, reflecting on CVS’s influence eight days after her Oak Street purchase closed. “You’re not going to get it right all the time,” she acknowledges. “But how do we get better?”

The business answer to those questions—for CVS, and for its entire industry—has been to get relentlessly bigger. Over the past two decades, Lynch’s onetime drugstore has snapped up storefront medical clinics; Caremark, the nation’s largest pharmacy benefit manager (or PBM); Aetna, the nation’s third-largest insurer; and now two new care businesses.

CVS is jockeying for these deals with a wide array of competitors, in health care and beyond. Rival mega-pharmacy Walgreens has invested billions of dollars in primary care clinic VillageMD and urgent-care operator Summit Health. Amazon just spent $3.9 billion on One Medical and its 200 doctors’ offices. Cigna bought PBM ExpressScripts for $67 billion in 2018. Health care groups and hospitals have been consolidating for years, and deep-pocketed private equity investors are snapping up providers of all kinds.

All of this activity is taking place in the long shadow of UnitedHealth Group (UHG), the nation’s largest insurer and largest employer of doctors. With $324 billion in 2022 revenue, it’s also larger by a smidgen than CVS. It has spent the past decade building Optum, its highly profitable health services juggernaut, whose businesses span from home health to surgical centers to claims processing tools, and cater to the entire industry, competitors included. (Optum’s model is now the go-to playbook for huge insurers: Elevance Health and Humana have both formed similar units.) Nor does UHG plan to stop expanding anytime soon. “Despite our size, we’re just scratching the surface of the opportunity,” CEO Andrew Witty told an investor conference audience in November.

“UnitedHealth has an entire ecosystem—and that’s what CVS and others are trying to replicate,” says Lisa Gill, head of health care services research at J.P. Morgan. The ultimate goal, she adds, is for each company to meet each patient’s every medical need—and “have the ability to drive them to the lowest-cost, best-outcome, most convenient care.”

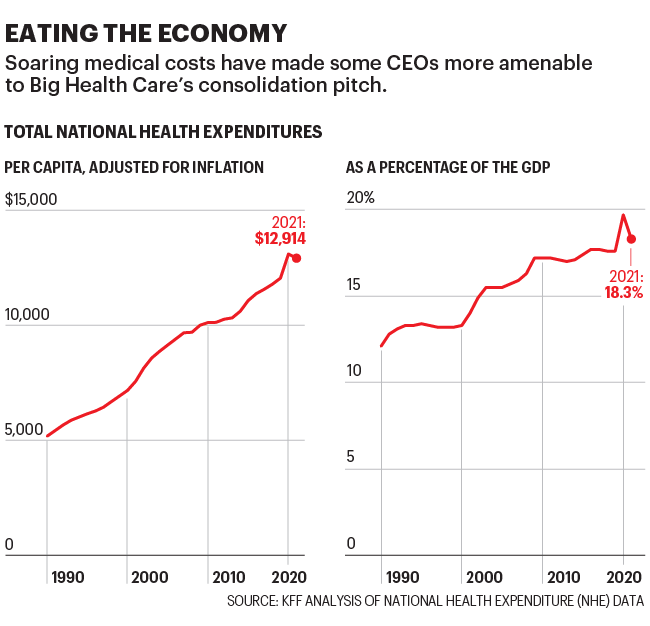

That goal resonates—especially after COVID, which made every American that much more aware of the flaws in our health care system. Everyone knows that system is broken. It’s ludicrously expensive: Health care spending reached $4.3 trillion in 2021, or $13,000 per person—almost a fifth (18.3%) of U.S. GDP. The costs are untenable for both individuals and their employers who provide insurance. And in the absence of Medicare for all, it has provided a broad opening for UHG, CVS, and their rivals to chase scale and profits in the name of building something better.

“Our growth has allowed us access to more of these capabilities,” says Dr. Margaret-Mary Wilson, UHG’s chief medical officer. She says the strategy is not about a pile of “flashy acquisitions” but about “bringing the pieces together to help drive value.”

Health care executives, investors, and some practitioners argue that this “vertical integration”—marrying primary care clinics and physicians’ practices to insurance, pharmacy benefit management, data analytics, and a host of related businesses—is, or will be, good for everyone. Companies can deliver care more efficiently and conveniently, providing more services to lower-income patients and other underserved populations, and heading off the chronic conditions and serious illnesses that drive up costs.

Insurers, accustomed to thinking in terms of cost control, say that they’re the right companies to run this new model. The hope is that a grateful nation will benefit both physically and financially and reward these companies with more business—creating the ultimate virtuous cycle.

As the industry embraces what it calls “value-based care,” the vision is a patient experience that involves seeing doctors and other providers early and often, in settings closer to (or sometimes even in) their homes. These low-stress, tech-enabled relationships will provide quick intervention, disease management, and wellness counseling, with the aim of preventing ER visits and hospitalizations. The biggest companies say that by rapidly growing, they can assemble the pieces to realize this vision.

Well, the growth is happening. Health care companies dominate business like never before: On the most recent Fortune 500 list, the industry accounted for eight of the top 25 largest U.S. companies by revenue. CVS and UnitedHealth earned 162% and 193% more revenue, respectively, in 2022 than they did in 2012. (CVS is also a sponsor of Fortune conferences and the Fortune Well health news site.) Cigna and Elevance grew by 520% and 154%, respectively.

But the broader benefits are, so far, a matter of debate—and the focus of much skepticism among doctors, patients, lawmakers, and industry critics. “Everything about the incentive structure that exists, when you have providers and insurers and pharmacy benefit managers coming together under one roof, to me spells ‘conflict of interest,’ ” says Sara Sirota, a policy analyst at the American Economic Liberties Project, a nonprofit focused on antitrust advocacy. “That’s going to harm services and prices for patients.”

The health care giants point to early signs of improvement, and promise even bigger benefits further down the road. In the meantime, they keep growing at a blistering pace. Which means it’s more urgent than ever to ask: Who benefits from Big Health Care’s growth—and will it really make America healthier?

Back in 2007, Southwest Medical Associates was practically an asterisk in news coverage of UnitedHealth Group’s $2.6 billion merger with Sierra Health Services, a Nevada-based insurer (and Southwest’s parent). That UHG was picking up a multispecialty practice that employed 250 providers appeared of little consequence compared with the company’s insurance gains—including a fatter tap into Nevada’s pool of Medicare-eligible retirees.

But with Southwest, UHG was beginning a far larger project than perhaps anyone appreciated, embarking on a journey to radical, next-level Bigness—with a propulsive strategy to not just manage payments for health care, but to deliver care, too.

UHG has since amassed a workforce of some 70,000 physicians and an untold number of advanced practice clinicians that work for Optum Health. That business complements two others—pharmacy benefit management (OptumRx) and data services (Optum Insight)—that now constitute Optum, the company’s $186 billion health services division. Optum has been bolstered by a series of audacious deals (see the below graphic), and analysts muse about it one day dwarfing UnitedHealthcare (UHC), UHG’s bread-and-butter insurance business.

Impressively, in building this many-tentacled colossus, UHG has turned many of its competitors into customers, forging complex relationships across the health ecosystem: UHC’s insurer rivals now depend on Optum’s data services and doctors, and UHC covers services offered by providers who are Optum Care’s competitors. “Like a lot of situations in the health care market, United was more forward-thinking,” says George Hill, an analyst at Deutsche Bank. “They were the first guys to plant the flag in the ground, realizing that care delivery could be the next large business in the space.”

Optum’s strategy broke from the industry convention of expanding “horizontally”—with hospitals acquiring hospitals and insurers acquiring insurers. UHG expanded “vertically” to seek more growth in part because years of horizontal acquisitions meant it had expanded into every insurance market it wanted to be in.

Another key driver for UHG’s strategy came in the Affordable Care Act. Embedded in that landmark legislation were measures designed to wring better value from the health system by rewarding quality of care. Insurers were also subject to a new regulation—the Medical Loss Ratio floor—that required they spend 80% to 85% of their premium income on medical care, effectively capping their profitability. For fatter margins, insurers would have to look for revenue elsewhere in the health care system.

That supercharged UHG’s foray into health services, and it has built that business with an eye toward efficiency—buying up surgical centers and urgent care clinics that can provide services more cheaply than hospitals, and bulking up on data-crunching tools to inform care-related decisions. Wilson, the chief medical officer, describes those pieces as the infrastructure for delivering and incentivizing value-based care.

Such care is rooted in the idea that much of what ails America’s miserably fragmented and expensive health system are the flawed incentives at its heart, the “fee-for-service” payment model that rewards providers for volume of care rather than good outcomes. The fix requires flipping those incentives on their head, encouraging the use of less-expensive services like primary care and preventative medicine, along with coordination tools that help keep people healthy.

The idea has wide support, but the concept has become muddled in practice. The term is now used loosely to describe an array of payment models where providers assume a degree of risk in providing care. These include the “capitated” (lump sum) payments in Medicare Advantage, a fast-growing business that in recent years has become the industry’s most profitable and highly prized. Of the 60 million people currently enrolled in Medicare, roughly half have signed up for Medicare Advantage programs—which are run by private insurers.

With an aging population and an attendant pot of revenue as an incentive, there’s suddenly a lot more energy behind the shift to value-based care. UHG has a larger, clearer vision, and Wilson acknowledges its heft helps in getting there: “One does need a critical mass of patients to execute on this [and] physicians collectively, to be open and willing to innovate with us.”

Dr. Tony Lin has spent his entire career at Kelsey-Seybold Clinic, a multispecialty practice in Houston. Since he joined in 1993, Kelsey has grown to include hundreds of doctors at 36 branches across the city. Kelsey earned a reputation for providing high-value care on a capitated model, receiving a lump sum to manage a patient’s health. The practice achieved good results by taking a team-based approach to care and by providing services like joint replacements and chemo infusions—often performed in hospitals at great expense—at a much lower cost in its clinics.

Lin, now Kelsey’s CEO, could promise employers on average 15% to 30% savings on health care spending. But when it came to bigger companies in the Houston market, that didn’t matter. They’d ask, “Who is Kelsey? What do you do? You only have 300 doctors?” and instead choose a national plan. To Lin, it was clear what he needed: “partners to get bigger.”

In April 2022 Lin hitched Kelsey to the Optum train. When Fortune visited Kelsey in mid-May, Lin said the relationship was still in the early stages—not much has changed for doctors on the front lines—but he felt fortified by the relationship: “We’re bigger, we’re more accessible. There’s more technology.”

Those tech resources include machines that can quickly screen for peripheral artery disease, allowing nurses to do in under five minutes a test that previously took 15 and was thus often skipped. Lin says Kelsey has tested 70% of its Medicare Advantage patients, a third of whom they discovered to be at risk. Those patients now receive a range of treatments, from care plans focused on diabetes and blood pressure control to discussions about lifestyle changes—interventions that Lin says can prevent more serious issues like claudication (muscle pain) or ulcers.

Leveling up also means providers have access to data analytics that can help stratify and target patients according to their risk of health setbacks, and to sort primary care physicians and specialists according to how closely they adhere to evidence-based medicine—all designed to steer patients to the most effective care.

Value-based care isn’t yet the norm at UHG. Of its insurance company’s roughly 50 million members, 15 million are under value-based arrangements; and of Optum’s more than 103 million patients, just 4 million get capitated care. But Lin says he values UHG’s commitment to the philosophy. Despite the enormous scale of Kelsey’s new owner, Lin still feels, in America’s fee-for-service-dominated health system, that he and his colleagues are the little guys. Joining forces with Optum, he says, “gives us a little more juice.”

Traditionally, doctors and insurers are at odds in a zero-sum standoff: The more you provide, payers say, the less I make. But in the move to value-based care, UHG saw an opportunity in putting providers and payers on the same team—an opportunity CVS and others are now also seizing.

The evolution of CVS beyond toothpaste and toilet paper began long before Karen Lynch arrived. In 2006, the pharmacy chain bought MinuteClinic, its first foray into storefront clinics; a year later, it paid $26.5 billion for Caremark, the country’s largest pharmacy benefit manager, which effectively sets drug prices for 110 million Americans.

More deals followed over the next decade, some more successful than others, but the M&A that brought Lynch in-house was the most consequential. In 2015, Lynch was named president of Aetna, after running the integration of its $7.3 billion purchase of Coventry, a Medicaid and Medicare insurer. Then, in 2018, CVS bought Aetna—and tasked her with merging its enormous operations into the pharmacy chain.

Overseeing that high-stakes corporate marriage put Lynch in line for the top role at CVS, and once she took the reins, she continued that company’s transformation. CVS supersized many of the in-store clinics it already operated in some of its 9,000 locations, as Lynch moved to expand more aggressively into primary care—the vital, if underfunded and short-staffed, front door for health care. “Consumers are seeking this type of relationship,” she told investors in late 2021. “We can be at the center of their care.”

That proposition is even more appealing when consumers come with government-guaranteed insurance. Lynch’s M&A strategy has zeroed in on providers whose patients are or soon will be eligible for Medicare and Medicare Advantage. Last year, Lynch set her sights on Signify Health, a Dallas-based company that sends doctors and other providers to the homes of elderly patients. After reportedly getting into a bidding war with UHG and Amazon, CVS in September agreed to pay $8 billion for Signify’s 10,000 providers and 2.5 million patients. “It’s kind of a throwback to the ’50s, where the doctor used to come to the home,” says Signify Health CEO Kyle Armbrester. “We can bring [care] in a convenient, accessible, preventative way.”

Lynch wasn’t done. Oak Street has a different model than Signify, but a similar patient base. It operates storefront clinics in lower-income urban neighborhoods and strip malls in 21 states, providing care to more than 225,000 seniors—more than half of whom are Black, Latinx, or Indigenous. In February, while waiting for the Signify deal to close, CVS agreed to pay $10.6 billion for Oak Street. Less than three months later, it was the proud owner of two big, Medicare Advantage–focused businesses.

Lynch still wants to buy digital health tools, to better connect CVS’s health care operations with consumers. But as she told investors and Fortune in early May, first she wants to focus on bringing Signify and Oak Street in-house, and cross-selling their services to more current or potential patients. “It’s like the renaissance of health care right now, where you see everyone moving to this value-based care using technology-enabled platforms,” Lynch says. “Now we’re all connected together.”

Lynch, Armbrester, and Oak Street’s Pykosz spoke with Fortune during a joint interview near West Palm Beach. It was the first time all three CEOs sat down with a reporter, a week after the Oak Street deal closed. During an hour-long conversation, Lynch was rarely the first to respond to questions, allowing the two younger men who had just become her newest direct reports to take first crack at promoting and defending their work. But all three stuck to the same message: Combining their separate businesses, to give CVS a larger piece of Americans’ health care spending, will give the nation what it needs. “I’m really proud of what we built—but that’s not moving the needle for the country,” Pykosz said. “CVS will allow us to grow, to reach more older adults—and to allow us to say we’re actually helping to solve societal problems.”

Over multiple interviews, Lynch consistently argues that chasing profits will also benefit patient welfare—even as she acknowledges that, as head of a huge public company, her first responsibility is to the bottom line. “While recognizing that we have shareholders, and a lot of different stakeholders, my personal passion is, ‘How do we improve the health care system?’ ” she says. “We have the opportunity to really drive engagement, simplicity, effectiveness—and to drive patients to the right care at the right time, in the right places.”

“While recognizing that we have shareholders, and a lot of different stakeholders, my personal passion is, ‘How do we improve the health care system?’“

Karen Lynch, CEO, CVS Health

Some argue that the biggest health care companies are too effective in the wrong ways. Federal and state lawmakers are concerned about the tremendous pricing control exerted by pharmacy benefit managers (PBMs), which they wield to keep their costs down and profits up. The three largest PBMs—CVS’s Caremark, Cigna’s Express Scripts, and UnitedHealth’s OptumRx— control about 80% of the market. In May, a U.S. Senate committee advanced a bill that would ban certain PBM pricing practices, while Florida Governor (and presumed 2024 Republican presidential candidate) Ron DeSantis signed a PBM reform bill into state law.

Lynch attributes this fervent regulatory wave to “a lack of understanding” about how PBMs “reduce pharmacy costs.” But doctors, patients, nonprofit experts, and pharma companies also criticize PBMs and their insurer owners for routinely refusing to fully cover drugs and devices that doctors consider medically necessary, including women’s contraception, when cheaper potential alternatives exist. The effect is to stifle innovation—and to limit the medical treatments available to all Americans, in the interests of restraining costs.

Many also see the nation’s devastating opioid crisis as a symptom of the industry’s elevation of financial efficiency over well-being. In November, CVS and Walgreens each agreed to pay about $5 billion, without admitting wrongdoing, to settle lawsuits over their pharmacists’ roles in filling opioid prescriptions. (Like the crisis itself, the related litigation has been ongoing since well before Lynch joined CVS.) Other health care giants—including drug distributors McKesson, AmerisourceBergen, and Cardinal Health—have reached similar settlements.

All these critiques come in the context of broader frustration, particularly among progressives, with decades of M&A. “The furious pace of consolidation in health care is resulting in higher prices and lower-quality care for patients,” Sen. Elizabeth Warren (D-Mass.) told Fortune in an email. FTC Chair Lina Khan has called health care “an area where we’ve seen so much consolidation across the entire supply chain, and what seems to be serious harm stemming from potential abuses of market power.”

Given that skepticism, CVS, which spent about six months jumping through regulatory hoops before it could finish buying Signify, expected similar scrutiny over the Oak Street merger. Instead, the FTC let the deal slide through in three months. Antitrust lawyers and Wall Street analysts were shocked. Even CVS itself, which was initially expecting the merger to take most of 2023 to finalize, was caught a little by surprise; it has announced that it will make less money this year than predicted, since it had suddenly moved the unprofitable Oak Street onto its books. (In May, CVS also took out a $5 billion loan, so it could pay Oak Street shareholders months earlier than expected.)

Not that Lynch is complaining in public. Now that she’s assembled the core pieces of CVS’s primary care pivot, she has the chance, and the challenge, to prove that her company can meaningfully improve the nation’s health care.

One of Oak Street’s newer clinics sits on a wide corner in Bushwick, the rapidly gentrifying hipster enclave in Brooklyn. On a recent sunny afternoon, the facility’s stately green-and-white signage—complete with an AARP endorsement—competed for attention with a teal-and-white urgent-care storefront across the street. Inside, past the receptionists, a large and airy (if empty) community room awaited seniors who, executives say, are welcome to come in to check email, meet for coffee, or enjoy the air conditioning—regardless of whether they need medical care.

The Bushwick location, one of 16 that Oak Street has opened in New York City in three years, is well-stocked and seemingly well-staffed. There are three on-site clinical providers, including two doctors who speak fluent Spanish—important in a neighborhood where more than half the population is Hispanic. “We find that many people who get care at Oak Street have sometimes not felt welcomed by the health care system—and we pride ourselves on really nice places where people can feel welcomed and supported,” says Dr. Marisa Rogers, an Oak Street executive medical director.

That’s if they can be enticed to walk in the door in the first place. During an hour-long midday visit, a Fortune reporter saw about 10 staff members—but crossed paths with no patients entering or leaving. (A spokesperson later confirmed that three patients had appointments during that time.) Pykosz says that emptiness is a feature, not a bug: “We actually really love when there’s no one in the waiting room, because that means everyone’s in their exam rooms,” he says.

Still, it’s safe to assume CVS didn’t buy Oak Street without wanting to fill its storefronts with more patients. Lynch, Armbrester, and Pykosz sketch out a future in which many of the 1,100 seniors who walk into each CVS pharmacy every week—some 8 million potential customers overall—are referred to Oak Street clinics for a wellness visit, or offered a home visit from a Signify doctor who can help them stay on track with medications.

Those pharmacy relationships could become invaluable pipelines for Signify and Oak Street. They could also help them overcome some of the scrutiny they’ve faced over their existing customer acquisition tactics. Patients have complained in online reviews to the Better Business Bureau about “relentless” telemarketing calls from Signify; meanwhile, Oak Street in 2021 disclosed that it was the target of a Department of Justice investigation around its marketing. (A spokesperson says Oak Street is complying with the inquiry.) “It is hard to reach seniors,” Armbrester says, “but we do that in a way that’s highly compliant .”

Most notably from a strategic standpoint, Oak Street and Signify focus on Medicare Advantage populations. That positions them, along with CVS, right at the center of some of the fiercest battles over integration and value-based care.

At the core of the conflict is the fact that capitation in Medicare Advantage is risk-based: That is, providers get larger sums to care for patients with more complex conditions. Makes sense, but the government alleges that many of the market’s largest players exploit that formula for profit by “overcoding” how sick their patients really are, defeating the purpose of value-based care. (“We disagree with any characterization of upcoding in our business,” an Oak Street spokesperson says by email.)

“We’ve got some important imperfections in those risk-adjustment systems,” says Dr. Mark McClellan, a former administrator for the Centers for Medicare and Medicaid Services who leads the Duke-Margolis Center for Health Policy. “You have an incentive to identify more diagnoses and get paid more that way.” A recent CMS rule, to be phased in over three years, aims to prevent the abuse with changes to the model.

In the meantime, the debate continues, and some of the industry’s early proof points—data suggesting that the integrated model is working—receive piercing scrutiny. At UHG, Wilson, the chief medical officer, celebrates Optum’s House Calls program, a service geared for its Medicare Advantage population, as a triumph of patient-centered, equity-enhancing medicine. In 2022, advanced practice nurses visited 1 million patients at home, at no charge, to conduct an evaluation and “environmental scan” in which their health and social needs were inventoried. UHG identified undiagnosed conditions in a quarter of the population, putting patients who had fallen through the cracks on track to receive care.

It’s an encouraging story. But it rests uneasily next to a 2021 report from the Department of Health and Human Services inspector general’s office that flagged home-based risk assessments as a way Medicare Advantage sponsors—UHC chief among them—maximized their payments. A UHC statement says the report “ignores the significant health benefits delivered by in-home clinical care.”

Observers are also split over how to interpret a peer-reviewed study that Optum researchers published on JAMA’s Open Network last December. The paper looked at the outcomes of more than 300,000 Medicare beneficiaries, half of whom were in two-sided risk Medicare Advantage plans (in which physicians gain financially if outcomes are good and lose if they’re bad), versus half in traditional fee-for-service plans. The Optum team found those in the MA plans were at significantly lower risk for hospital admission (–18%) and emergency room visits (–11%), among six other improved quality metrics.

The MA patients were also found, however, to have much higher rates of comorbiditi—33% had been diagnosed with diabetes, compared with 23% in the fee-for-service population, and they were more than twice as likely to be coded as having kidney or lung conditions. UHG argues that these patients’ conditions were legitimately diagnosed thanks to Medicare Advantage’s model, avoiding complications and expense down the road. It also notes that CDC figures estimate 29% of adults have diabetes. But critics see the disparities as proof of upcoding, emerging yet again.

The promise of value-based care has been a pot of gold at the end of the health care rainbow that policymakers, innovators, and business leaders have chased for years. But now, with the largest, most profitable health care companies more boldly jostling for opportunity and touting early success, there’s some awkward ambivalence among value-based care’s early champions. In conversations with a couple dozen stakeholders, including three former CMS administrators, about Big Health Care’s fitness for the value-based care role, most opinions landed between skeptical and wait-and-see. Will care improve? Maybe, through better coordination. Will it lower costs? Unlikely. Is investment in primary care, whatever the source, a good thing? You bet.

“Insurers are arguing it gives doctors a chance to become part of integrated care, and build more supportive systems,” says Donald Berwick, another former CMS administrator. “I think the evidence is not there right now.” Doctors, he says, are demoralized: “They want to work for patients, and now they find that working for financial interests … it’s a toxic trend that we’re going to pay dearly for.” Indeed, to the extent that consolidation squeezes doctor compensation, it may be self-defeating—since that will mean fewer medical practitioners, at a time when an aging population arguably needs more.

Elizabeth Mitchell, CEO of the Purchaser Business Group on Health, a coalition of the nation’s largest employers, argues that consolidation—horizontal or vertical—has been working to the detriment of her member organizations for years: “All of the evidence shows that it does not improve quality or patient experience, but it absolutely drives up prices.”

“The incentives are not super strong for these companies to actually do a great job of lowering costs,” says Dave Windley, a Jefferies analyst, who notes that from an investor’s perspective, shrinking insurance-side revenue is “like stunting one’s own growth.” But experts also concede that the impacts of vertical consolidation, of the sort CVS and UHG are pursuing, are less well understood, in part because it’s newer, and the companies haven’t been very transparent.

The common takeaway is that Big Health Care has much work to do in gaining trust—among health care practitioners and patients alike—and in proving that its business models are as healthy for society as they are for their bottom lines.

To which the response of the giants seems to be: Give us a little more time. Looking ahead after CVS’s buying spree, Lynch sounds as if she knows the burden of proof is on her industry. “We’re making progress, we did what we said we would,” she says. “And we now have to make all those connections.”

Editor's note: This article has been updated to provide attribution for information related to CVS's acquisition of Signify Health.

A version of this article appears in the June/July 2023 issue of Fortune with the headline, "Big health care's big test."